All Categories

Featured

Table of Contents

A PUAR enables you to "overfund" your insurance coverage plan right up to line of it coming to be a Modified Endowment Contract (MEC). When you make use of a PUAR, you quickly increase your money worth (and your survivor benefit), therefore boosting the power of your "bank". Additionally, the more cash worth you have, the greater your interest and reward settlements from your insurance business will be.

With the increase of TikTok as an information-sharing system, monetary suggestions and strategies have found a novel way of spreading. One such method that has actually been making the rounds is the infinite financial idea, or IBC for short, gathering endorsements from celebrities like rapper Waka Flocka Fire. While the technique is presently popular, its roots map back to the 1980s when economist Nelson Nash introduced it to the world.

Who can help me set up Financial Leverage With Infinite Banking?

Within these policies, the cash worth expands based on a rate established by the insurance firm (Tax-free income with Infinite Banking). Once a substantial cash worth gathers, insurance policy holders can get a cash value lending. These finances differ from traditional ones, with life insurance serving as collateral, implying one could shed their insurance coverage if loaning exceedingly without sufficient cash value to support the insurance policy prices

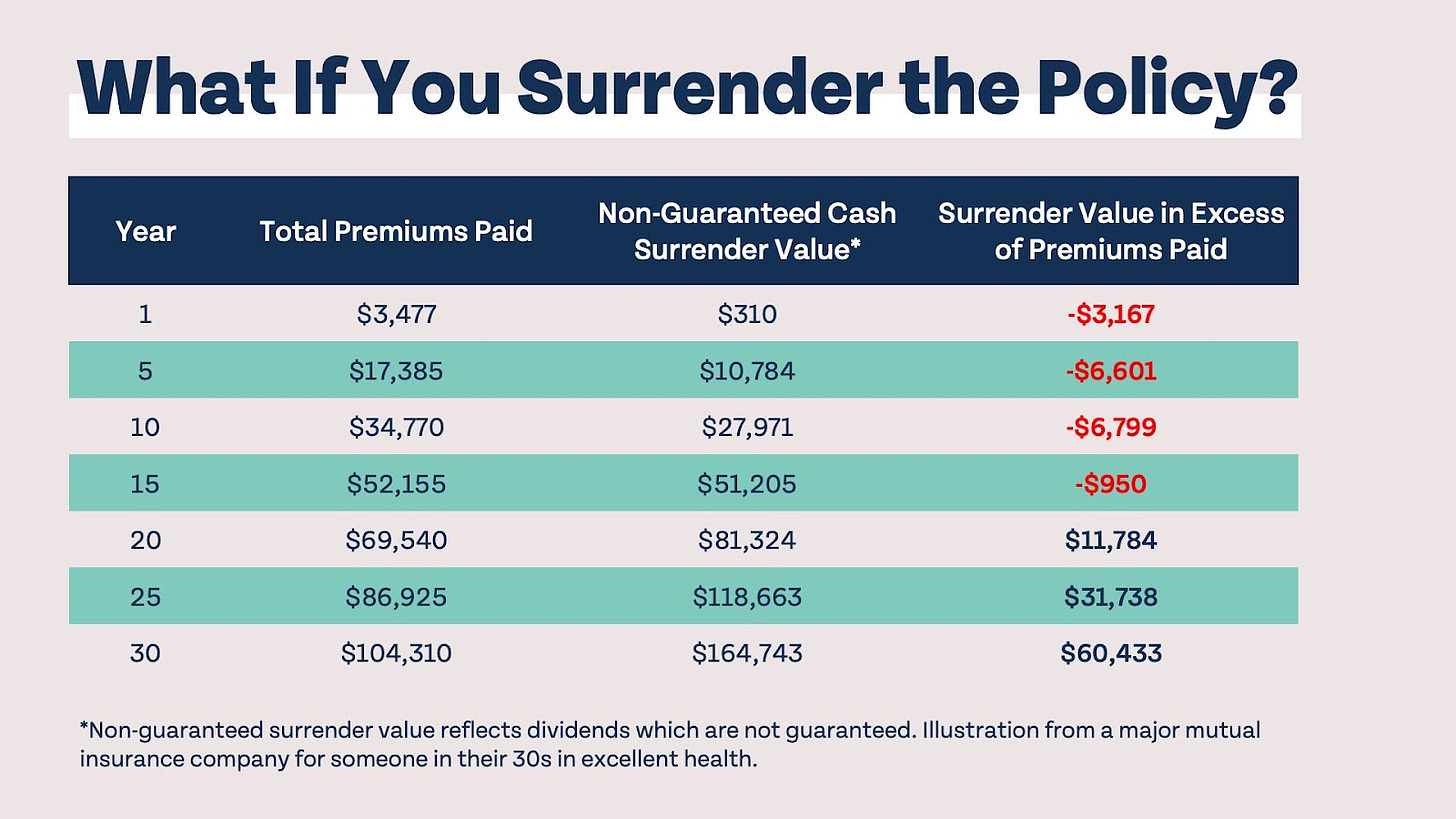

And while the allure of these policies appears, there are innate constraints and dangers, requiring diligent cash value tracking. The technique's authenticity isn't black and white. For high-net-worth individuals or entrepreneur, specifically those utilizing techniques like company-owned life insurance coverage (COLI), the advantages of tax breaks and compound growth might be appealing.

The appeal of limitless financial doesn't negate its obstacles: Expense: The fundamental requirement, a long-term life insurance coverage plan, is costlier than its term counterparts. Qualification: Not every person gets approved for entire life insurance policy due to rigorous underwriting procedures that can exclude those with specific health or way of life conditions. Complexity and danger: The detailed nature of IBC, combined with its dangers, might prevent several, specifically when easier and much less high-risk alternatives are available.

How do interest rates affect Infinite Banking?

Designating around 10% of your regular monthly earnings to the plan is simply not practical for a lot of people. Part of what you review below is simply a reiteration of what has actually already been stated over.

So prior to you get yourself into a circumstance you're not gotten ready for, recognize the adhering to initially: Although the principle is commonly offered as such, you're not in fact taking a car loan from on your own. If that were the case, you wouldn't need to settle it. Rather, you're obtaining from the insurance provider and have to settle it with rate of interest.

Some social media blog posts recommend utilizing cash worth from entire life insurance policy to pay down credit history card financial obligation. When you pay back the financing, a section of that passion goes to the insurance coverage company.

For the initial several years, you'll be paying off the payment. This makes it very hard for your policy to build up value throughout this moment. Entire life insurance policy costs 5 to 15 times much more than term insurance policy. Many people simply can't afford it. Unless you can afford to pay a couple of to several hundred dollars for the following years or even more, IBC won't work for you.

What type of insurance policies work best with Infinite Banking In Life Insurance?

Not everybody must rely only on themselves for economic safety and security. If you require life insurance policy, right here are some useful suggestions to take into consideration: Think about term life insurance policy. These plans provide protection during years with significant economic commitments, like mortgages, trainee fundings, or when looking after children. Make certain to look around for the finest price.

Picture never having to stress concerning financial institution lendings or high passion prices again. That's the power of infinite banking life insurance coverage.

There's no set funding term, and you have the liberty to pick the settlement routine, which can be as leisurely as paying back the loan at the time of fatality. Infinite Banking concept. This flexibility includes the servicing of the fundings, where you can choose for interest-only payments, keeping the car loan equilibrium level and manageable

Holding money in an IUL dealt with account being attributed rate of interest can usually be better than holding the cash money on deposit at a bank.: You have actually always desired for opening your own bakery. You can obtain from your IUL policy to cover the first expenses of leasing an area, acquiring devices, and working with personnel.

How does Cash Flow Banking compare to traditional investment strategies?

Individual car loans can be obtained from typical financial institutions and credit rating unions. Borrowing money on a debt card is typically very pricey with yearly percent rates of rate of interest (APR) usually getting to 20% to 30% or even more a year.

{kind=link}

Latest Posts

Wealth Squad Aloha Mike On X: "Become Your Own Bank With ...

Be Your Own Banker Nash

Life Rich Banking